EMI Options

When we buy goods, some banks provide us with the EMI option, which allows us to pay the amount in equal monthly installments. The complete form EMI is “Equally Monthly Installment.”

Let’s study EMI in detail here.

What is EMI?

EMI is short for Equated Monthly Installment. It's a method of paying for an expensive thing by dividing the cost into small, uniform payments made on a monthly basis.

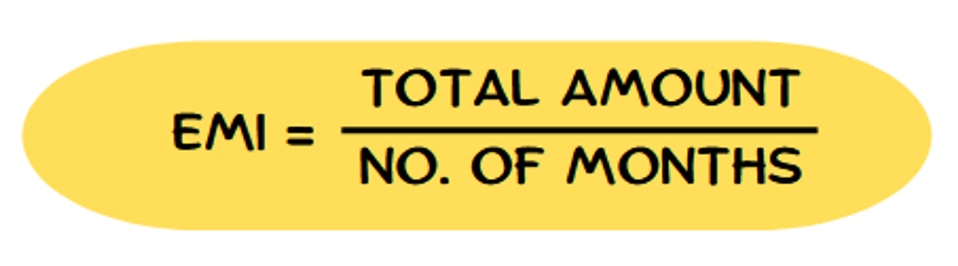

Definition of EMI:

Suppose you wish to purchase a toy worth ₹1,200 but do not have the entire amount available with you. Rather than waiting until you can save ₹1,200, you can pay ₹100 monthly for 12 months. This is referred to as EMI, which is paying in installments each month.

The EMI is calculated by dividing the total amount by the number of months.

Suppose you bought an almirah for Rs 20,000 and want to go for the EMI option for 10 months.

Then each month, you have to pay Rs (20,000 ÷ 10) = Rs 2,000.

Types of EMI Options

Various categories of EMI plans fit diverse requirements. Let's discuss them:

1. Normal EMI (With Interest)

-

Definition: You take a loan to purchase something and promise to repay it in the same amount each month over a definite time, with interest.

-

Example: If you take a loan of ₹10,000 at an interest of 10% per year for 12 months, your monthly EMI will be more than ₹833 due to the interest charged.

-

Fun Fact: The longer you repay, the greater the interest!

2. No-Cost EMI

-

Definition: You only pay the true price of the object, broken down into monthly payments, without any additional interest fees.

-

Example: A gadget priced at ₹12,000 can be paid in 12 monthly payments of ₹1,000 with no interest.

-

Fun Fact: This is sort of like a present from the seller, where they pay the interest on your behalf!

3. Debit Card EMI

-

Definition: You can finance your purchase using your debit card by converting it into EMIs and paying through direct deduction from your bank account.

-

Example: Purchasing a ₹5,000 phone and paying ₹500 per month for 10 months.

-

Fun Fact: Not everybody can do this; banks verify if you're qualified!

4. Buy Now, Pay Later (BNPL)

-

Definition: You receive the product instantly and pay later, typically within a brief time frame like 15 or 30 days.

-

Example: Purchasing a ₹2,000 book and paying ₹2,000 in 30 days.

-

Fun Fact: Zero interest for timely payment is available in some BNPL plans!

5. Credit Card EMI

-

Definition: With your credit card, you can pay for your purchase in EMIs, where the amount is charged monthly.

-

Example: buying a ₹15,000 tablet for ₹1,500 per month for 10 months.

-

Fun Fact: There are credit cards that provide EMI conversion at the point of purchase!

How EMI Works: A Simple Calculation

Let us learn the calculation of EMI through a simple formula:

Where:

-

P = Principal loan amount

-

r = Monthly interest rate

-

n = Loan tenure in months

Example:

-

Loan Amount (P): ₹12,000

-

Annual Interest Rate: 12%

-

Loan Tenure: 12 months

Convert the annual interest rate to a monthly interest rate:

Now, calculate the EMI:

So, the monthly EMI would be approximately ₹1,061.11.

Solved Question: EMI Calculation

Question:

Ananya wants to buy a bicycle worth ₹6,000. She decides to pay in 6 equal monthly installments. How much will she pay every month?

Solution:

Answer:

Ananya will pay ₹1,000 every month for 6 months.

Advantages And Disadvantages Of EMI

Advantages of EMI

-

Affordability: Compresses expensive products into a more affordable offering by dividing the cost into smaller installments over time.

-

Budgeting: Facilitates effective planning of monthly expenditure.

-

Immediate Access: Provides instant access to the product while paying in installments.

-

No Large Upfront Payment: Avoids the necessity of saving a huge sum before buying.

Disadvantages of EMI

-

Interest Charges: Certain EMI plans come with interest charges, which add to the total amount.

-

Financial Burden: Demands fixed monthly payments, which could be a strain on finances.

-

Eligibility Criteria: Not all individuals may be eligible for particular EMI plans.

-

Potential Debt: Failure to pay could result in debt accumulation and impact credit scores.

Tips for Managing EMI Effectively

-

Opt for Shorter Tenures: Lesser repayment tenure means lower interest paid.

-

Maintain Budget: Make sure the EMI fits into your budget for every month.

-

Avoid Multiple EMIs: Using too many EMIs can cause financial pressure.

-

Timely Payments: Pay in time to prevent fines and a healthy credit score.

Fun Facts About EMI

-

EMI for Toys: EMI plans are available for pricey toys at some toy shops!

-

EMI on Gadgets: Gadget items such as mobile phones and laptops can be purchased on EMI.

-

EMI During Festivals: Some stores provide special EMI schemes during festival seasons such as Diwali and New Year.

EMI in Real Life: A Story

Meet Aarav:

Aarav wants to purchase a new bicycle worth ₹8,000. Aarav currently does not have all the cash at hand, but he chooses to pay ₹1,000 per month for 8 months. This way, he can use his new bicycle immediately and repay it over a period of time.

Moral of the Story

EMI lets you indulge in what you desire today and pay for it in easy installments.

Conclusion

EMI is a useful tool through which you can purchase products you require or desire without being required to pay the entire cash amount. By knowing how EMI functions, its types, EMI advantages and disadvantages, and how to handle it judiciously, you can make judicious financial choices.

Remember, EMI is like a bridge between saving for something and enjoying it today. Always choose EMI plans that fit your budget and ensure timely payments to avoid any financial strain.

Common Misconceptions About EMI

Misconception 1: "EMI means no extra cost."

Truth: Only No-Cost EMI has no interest. Most regular EMI plans include interest, increasing your total payment.

Misconception 2: "Anyone with a debit or credit card can get EMI."

Truth: Banks check eligibility based on credit history, account activity, or credit card limits.

Misconception 3: "EMIs are only for big items like cars or houses."

Truth: EMIs are available for gadgets, appliances, toys, and even books, depending on the seller and the bank.

Misconception 4: "Skipping one EMI won’t matter."

Truth: Missing even one EMI can hurt your credit score and attract penalties.

Misconception 5: "BNPL and EMI are the same."

Truth: BNPL (Buy Now, Pay Later) typically offers a shorter payment period (15–30 days) and may not have interest if repaid on time, whereas EMI spreads the cost over several months.

FAQs:

1. What are the EMI options?

There are several EMI options available depending on the product, bank, and payment method:

-

Regular EMI (with Interest): You pay monthly installments along with interest.

-

No-Cost EMI: You pay only the product price in equal monthly parts, without extra interest.

-

Credit Card EMI: Convert your credit card purchase into EMIs.

-

Debit Card EMI: Eligible customers can pay in EMIs using their debit cards.

-

Buy Now, Pay Later (BNPL): Get the product instantly and pay later, often interest-free if paid on time.

-

Consumer Durable Loans: Offered by finance companies at stores for gadgets or appliances.

2. How does an EMI option work?

An EMI option works by breaking the total cost of a purchase or loan into equal monthly payments over a specific time period. Each EMI typically includes:

-

Principal: The actual amount borrowed or product price.

-

Interest: Additional cost charged by the lender (unless it's a no-cost EMI).

-

Tenure: Duration of repayment (e.g., 3 months, 6 months, 12 months).

The amount is auto-deducted monthly until the full repayment is done.

3. What is the easy EMI option?

The "easy EMI option" usually refers to EMI plans that are:

-

Interest-free or low-interest (like No-Cost EMI)

-

Quick to approve (such as BNPL or Debit Card EMI)

-

Conveniently available at the point of purchase (online or in-store)

These are designed for hassle-free purchases without heavy paperwork or long wait times.

4. What does EMI stand for?

EMI stands for Equated Monthly Installment.

When you choose "EMI options," you're selecting from different ways to repay the amount in equal monthly payments, including:

-

No-Cost EMI

-

Credit Card EMI

-

Debit Card EMI

-

BNPL (Buy Now, Pay Later)

-

Bank Loan EMI

Each option varies in terms of interest, eligibility, and repayment flexibility.

For more such math concepts, do visit the Orchid International Schools website.

Related Links

CBSE Schools In Popular Cities

- CBSE Schools in Bangalore

- CBSE Schools in Mumbai

- CBSE Schools in Pune

- CBSE Schools in Hyderabad

- CBSE Schools in Chennai

- CBSE Schools in Gurgaon

- CBSE Schools in Kolkata

- CBSE Schools in Indore

- CBSE Schools in Sonipat

- CBSE Schools in Delhi

- CBSE Schools in Rohtak

- CBSE Schools in Bhopal

- CBSE Schools in Aurangabad

- CBSE Schools in Jabalpur

- CBSE Schools in Jaipur

- CBSE Schools in Jodhpur

- CBSE Schools in Nagpur

- CBSE Schools in Ahmednagar

- CBSE School In Tumkur

Orchids The International School is one of India's leading chains of CBSE and ICSE schools, with 100+ schools across the country.